by Jim Scarantino | Mar 31, 2025 | General

Port Townsend’s grandiose, extravagantly expensive vision for Evans Vista contravenes the wisdom of the Strong Towns and Smart Growth movements. The project has hit a brick wall of economic reality, which provides an opportunity to get things right.

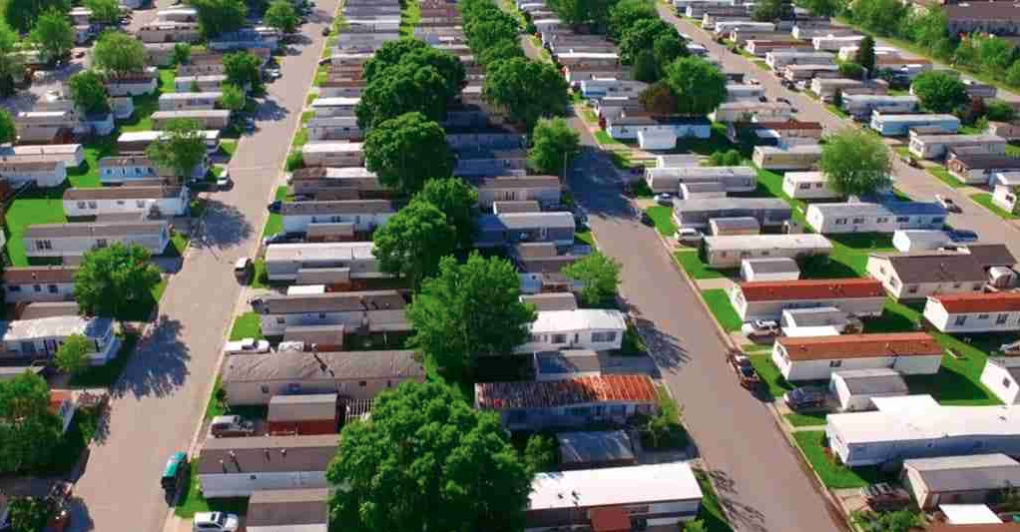

Manufactured housing is the only practical way to create affordable housing. Pre-engineered, pre-fabricated housing offers a path forward at Evans Vista. Other communities are embracing this answer to their housing crisis. It is time Port Townsend got real and embraced a solution right in front of us.

In my article, “Evans Vista Doesn’t Pencil Out, No Affordable Housing Coming Soon,” I discussed why the city’s $111-126 million (and counting) master plan for its 14.4 acre Evans Vista property is unfeasible. It is just too expensive to build. In this article I will discuss alternatives to the city racking up another affordable housing flop.

Ignoring Low-Hanging Fruit

Before the city purchased the Evans Vista property, it had already installed sewer and water infrastructure in that area adequate to serve 100 homes. At its 12/6/2021 briefing on the project, City Public Works Director Steve King told city council that no off-site street improvements would be required. There was “good water supply — no problem with fire flow or access to water.” And a two-inch sewer line already had been extended to the area.

This briefing occurred before council approved the purchase. The primary objective driving the acquisition and subsequent development was, according to the subtitle of King’s presentation, “Supply of Affordable Housing with Land and Architecture.” Fifty affordable units (meaning affordable to households making 80% of the area median income) were foreseeable, with another 50-100 workforce housing units. In other words, most of the goals of the proposed project could be attained with the existing infrastructure.

This pragmatic goal was jettisoned a few years later after the city paid an architectural firm nearly $500,000. What started as an attempt to create much needed low-cost housing morphed into a grandiose master site plan to develop a village of multi-story apartment buildings, townhomes, retail shops and other structures, complete with a daycare center, dog park, amphitheater and other amenities. Economists hired by the city to judge the feasibility of the plan told the council it was too expensive to build. City council voted unanimously to approve the plan anyway.

The stated purpose of approving that plan was to allow city staff to apply for land use amenities, such as platting. But city staff have not done that. Late last year, council authorized the city manager to spend another $160,000 in an attempt to interest developers in maybe biting off smaller pieces which were not in any way tied to the unfeasible grandiose half-million dollar master site plan. There’s been no word on response to that marketing pitch.

The city’s most ambitious foray into the housing market was not even mentioned at the 2025 State of the City address until audience members asked about it. See our article: “Correcting Mayor Faber on Evans Vista, PT’s ‘Meth Meadows,'” PTFP 3/16/25.

Nothing on the ground has happened except for (1) clearing homeless addicts and their debris from the forested area and (2) the emergence of an even larger, more dangerous homeless addicts’ encampment in the Evans Vista meadow. That camp has grown in the few weeks since my last article on this topic.

Unburdened of what has been, the city can start afresh. A manufactured housing community at Evans Vista could restore the original intent of the project and possibly deliver a 100% affordable housing project.

The featured photo above shows what a 100-unit community of manufactured trailer-style homes might look like. There is a chance of getting that built, but not the design below for which the city shelled out half a million bucks:

Be Strong and Smart

Let’s go back ten months before council voted to approve the purchase of Evans Vista, to a February 2, 2021 meeting of the Intergovernmental Collaborative Group (ICG). The ICG is comprised of the Jefferson County Board of County Commissioners, the City of Port Townsend, Port of Port Townsend, and Jefferson County Public Utility District. The purpose of the meeting, broadcast live on KPTZ, was to hear from Charles Marohn, founder and president of Strong Towns, and author of Strong Towns: A Bottom-Up Revolution to Rebuild American Prosperity.

Strong Towns works to help urban leaders and activists “learn why your city is going broke, gain the knowledge needed to stop bad development practices, have a plan to make your neighborhood stronger and more prosperous, and take control of your community’s future.”

Marohn’s presentation can be boiled down to a couple of points:

- Strong, prosperous, resilient, sustainable and financially-strong communities do not emerge from complicated top-down planning. They arise from incremental adaptation.

- What looks like chaos is evolution in process. “Order emerges from complex adaptation,” he emphasized. “What doesn’t necessarily pass the eye test” — meaning, buildings or streets that don’t look tidy, perfect, planned and coordinated — “actually profit the community” and pay positive returns.

Marohn advocated emulating poorer communities that focus on “getting it done” instead of the drawn-out, sometimes exhausting public engagement culture of western Washington. He encouraged chasing “the next level of density” at every opportunity and treating incremental growth “with the least amount of regulatory friction.”

Marohn’s presentation was warmly received. Some of the official audience, you could say, were gaga over the guru of urban policy. His emphasis on proceeding incrementally, with a light hand, with minimal top-down control, was applauded. Many of the officials claimed they were strong adherents to the Strong Towns approach and had been following the group’s work for years.

Strong Towns has many success stories. Its wisdom is being adopted across the country. But not in Port Townsend. Everything Marohn had to say went out the window in less than a year.

Not Smart Growth, Either

The city has been pursuing sprawl under the cover of adding affordable housing. We have been told that any construction at Evans Vista must wait until a sewer pump station is built at Mill Road. This would bring infrastructure to the Mill Road permanent homeless camp and beyond to Glen Cove, where the city would promote even more expansion and development. It is no secret that City Manager John Mauro wants the city to annex those areas.

Not only does this vision contravene the teachings of Strong Towns, it is not Smart Growth. The Smart Growth school of urban planning shares some of the same goals as Strong Towns. It also wants to keep cities from going broke and not repeating the mistakes of the Suburban Experiment.

“[D]eveloping within existing communities — rather than building on previously undeveloped land — makes the most of the investments we’ve already made in roads, bridges, water pipes, and other infrastructure, while strengthening local tax bases and protecting open space,” insists Smart Growth America. (By way of full disclosure, I was one of the early members of 1,000 Friends of New Mexico, that state’s smart growth organization).

The city has many, many acres of buildable land within its existing infrastructure boundaries. The city itself owns many parcels, including the still-empty site of the former Cherry Street affordable housing project, where infill could occur and take advantage of in-place streets, sewers, water lines and stormwater measures. One of those buildable areas already served by city infrastructure are the level acres at Evans Vista.

9-1-1? We Have An Emergency!

Disaster strikes. Homes are destroyed. What do emergency response agencies do to address the resulting housing emergency? They use manufactured homes. But in Port Townsend, the town leaders opt for fantastically expensive, impractical and rather snooty solutions, none of which they have managed yet to build.

Chalk it up to snobbishness? Does Port Townsend want affordable housing only so long as it does not look too affordable? Is it the grip of realtors on local government, realtors who don’t want to see a “trailer park” at the city’s entrance, even though it would make a huge impact on the city’s affordable housing crisis? Or is it simply that city leaders are stuck in the past and uninformed — self-proclaimed progressives who are actually resisting progress?

With the Cherry Street “affordable” housing project the city tried barging a 70-year old small apartment building from Victoria, B.C. You could say this was the city’s version of pre-engineered, pre-fabricated housing. I remember glowing talk of the hardwood accents inside and the building’s “bottle-dash” style of stucco application. After millions of dollars down the drain and years lost, only rats and raccoons found housing. The city eventually gave up and tore the building down.

Then the city promptly shelled out nearly $500,000 for architects to come up with a design supposed to bring affordable housing to Evans Vista. They got a utopian dream too expensive to build. Hey, but it had art plinths and an amphitheater!

Mayor David Faber has said the city is now “waiting for the stars to align” to move forward at Evans Vista. In addition to cursing the cosmos, he blames interest rates and a “spicy” situation in Washington, D.C.

Instead of surrender, I suggest the obvious: Rely on affordable structures that can be delivered and installed quickly.

Embrace the incremental approach city leaders claimed to admire when they applauded the teachings of Strong Towns. Take advantage of the ability that exists now to get a significant number of residential units at Evans Vista. And take the fastest, least expensive, most immediately impactful route — just as first responders do when responding to an emergency.

Instead of throwing money at architects, open the doors to those who are already providing affordable housing at scale across the country. That is the manufactured housing industry — the greatest source of unsubsidized housing in America. About 22 million Americans live in manufactured housing. Most of those live on less than $40,000 annually.

The industry is exploding and constantly innovating to meet growing demand. Manufactured housing communities — including mobile home parks — are “strong” communities, says Strong Towns. Some Habitat for Humanity groups have acquired mobile home properties and become licensed manufactured home dealers, allowing them to sell directly without any middle-man markup.

“We see manufactured housing as an important component to addressing the larger U.S. affordable housing crisis,” says Jim Gray, senior fellow at the Lincoln Institute of Land Policy. The Lincoln Institute sponsors the Innovations in Manufactured Homes (I’m HOME) Network. It brings together nonprofits, the private sector, and government agencies “to solve problems that are keeping manufactured housing from reaching its potential in the market,” says Gray, who led the Duty to Serve program at the Federal Housing Finance Agency (FHFA) before joining the Lincoln Institute.

Preserving manufactured housing communities is one of the 2025 legislative priorities of the Association of Washington Cities. The City of Port Townsend “actively supports” the Association’s agenda. Port Townsend has a chance to do more than cheer from the sidelines. It has a chance at Evans Vista, right now, to create the very kind of affordable, strong, resilient manufactured housing community acknowledged as a proven strategy for providing affordable housing.

Follow the recommendations of Strong Towns. Emulate less privileged communities to “get things done.” Scrap the interminable, exhausting public meeting process — playing Santa Claus to “the stakeholders” — that wastes time and resources. Reduce regulatory friction to a bare minimum.

Throw the doors wide open to manufactured home community developers and operators with this simple request:

“Tell us what you can do to provide manufactured housing at Evans Vista in the fastest, least costly manner. We will provide the land. What can you do, at what cost and how fast?“

With almost all infrastructure in place, the fastest, least expensive route is probably installing pads and hook-ups for mobile and manufactured homes. Concrete pads might be unnecessary for certain types of manufactured housing (see below). With the city providing the land on a minimal payment, long-term lease or via a land trust model, companies that create and manage manufactured home communities would have a hard time not considering the opportunity.

The city could ensure long-term affordability by stipulations in the agreement covering use of the land. Individuals could bring their own homes to the pads. Entrepreneurs could provide the structures and then lease them at affordable rates. There should be no aesthetic requirements, no exclusion of manufactured housing types, and no prohibitions against previously used structures.

Let the community grow organically, to apply an overused term. Let it adapt and evolve over time as strong towns do. First, maybe twenty manufactured homes of various types. Then another twenty, and so on — the development growing in response to the market and to individual wants and needs. Being pragmatic about Evans Vista, which is far from the most desirable parcel in the city, this approach may be the only way forward.

As for those looking down their noses at “a trailer park,” there should be no objection to a manufactured housing community since the city has permitted the use of manufactured housing as ADUs in upscale Uptown. Anyone keeping up with the industry knows that today’s manufactured homes are in many ways superior to stick-built housing.

Manufactured home companies and the lending industry have made it easier to finance manufactured homes. First Fed bank in Port Townsend, for example, praises manufactured housing as an alternative for those priced out of the traditional market. It backs up that conviction with a strong financing program. Some of the larger manufacturers, like industry leader Cavco, have their own financing programs.

No Alternative But Manufactured Housing

In addressing our housing crisis, the city should actively support the efforts of the Building Industries Association of Washington to roll back the onerous building code and other regulatory obstacles that make new construction unaffordable. According to the BIAW, almost 30% of the cost of new home construction comes from government regulations.

The adverse impacts of onerous regulations are magnified up and down the chain. “Climate change” regulations add greatly and unnecessarily to this price inflation, such as the requirement for EV chargers in newly constructed homes. The city has to decide whether it wants to get serious about a crisis impacting lives and depressing its economy now — the affordable housing crisis — or sacrifice affordable housing on the altar of woke ideology.

That said, the prospect of any real, substantial relaxation of Washington’s onerous regulations on new home construction is not very hopeful. Until a sea change occurs in the state’s and city’s political and ideological culture to get government off the backs of home builders and home buyers, the only way to provide affordable housing will be with manufactured housing.

The numbers don’t lie. BIAW reports that the average cost in Washington for a new single home is $309/sq.ft. This results in a median sales price in the Puget Sound of almost $700,000 — far above the national average. The cost for a new townhome — the supposed affordable option — is $404/sq.ft. The costs for multi-story apartment buildings such as those in the grandiose Evans Vista Master Site Plan go even higher.

The average cost of a manufactured home nationally is less than $150,000. BOXABL, a Las Vegas, Nevada manufacturer, is driving the cost even lower, offering a 361/sq.ft. Casita model for $60,000 (excluding land, utility hookups and shipping). These homes come standard with full kitchen and bathroom, as well as 9’6″ ceilings. At $166/sq.ft., the Casita provides high-quality structures at nearly half the average cost per square foot for a new single home in Washington state. Upon delivery, using standard flatbed trucks which can carry several folded-up future homes at once, they can set up in a few hours.

Interior of BOXABL Casita

A developer in Desert Hot Springs, California is using BOXABL Casitas along with other small options like tiny homes on wheels to build out a 90-home affordable community. Lots are 50 feet long by 25 feet wide, resulting in significantly greater housing density than in most areas of Port Townsend. Many mobile home parks have lots of 50 feet by 100 feet, requiring an acre for 9 units. An acre could accommodate 35 BOXABL Casitas, increasing density almost fourfold with just single-story structures.

BOXABL also produces larger structures, even apartment buildings. At the other end of the spectrum, it offers a “Baby Box” at an introductory price of $19,999. This tiny home is built to high standards and can be set up by one person in an hour. It is anticipated to require little to no permitting, little site preparation and no foundation. It comes standard with equipped kitchen, bathroom, dining area, pull-out bed, AC and heating system, and storage. It has water and waste storage tanks for off-grid living.

Why not allow off-grid living at Evans Vista in safe, warm structures? Do we have a housing emergency or not? Besides, dozens of people are already living there, off the grid, in soggy tents and unhealthy conditions, rather than in comfortable, state-of-the-art quarters.

BOXABL is but one example of the rapid innovation in manufactured housing that is driving prices lower while increasing quality. The manufactured and prefab home shows around the country unveil new designs and advances constantly.

One important advance is the ability to build multi-story prefab, pre-engineered homes, such as Wolf Industries of Battle Ground, Washington is doing. The ease of their approach can be seen in this video of their project in Aberdeen, Washington.

[youtube https://www.youtube.com/watch?v=TzjOMD–bGM&w=764&h=434]

Some architects don’t like these companies. They and others professionals don’t make money on “soft costs” when pre-engineered, pre-fabricated structures are used. At times they will actively steer clients away from and keep them ignorant of less-expensive, less time-consuming alternatives. That’s something I learned serving on the county’s pool task force when we evaluated “pre-fab, pre-engineered” aquatic pools and buildings that could produce savings of more than 50% over the city’s big bucks Taj Mahal architectural design.

At the “Evans Vista master plan kickoff” (2/21/23) the city’s architect, responding to questions from council member Ben Thomas about the possibility of using manufactured housing to achieve a quick, less expensive delivery of housing, promised to consider going that route. No one should be surprised that promise was not fulfilled.

The city should take this opportunity to embrace a disruptive technology that makes housing more accessible and affordable. Evans Vista is a perfect site for the city to showcase itself as a pragmatic innovator. The first thing the city should do is change the zoning at Evans Vista to allow detached single-family manufactured homes. As things stand, the city is zoning out the best chance for affordable housing that land may see for many years to come.

The next thing the city should do — itself, not through anyone associated with an architect — is get on the phone to manufacturers of pre-fab, pre-engineered housing and the companies that develop and manage manufactured housing communities. That should have been done years ago. Do it now.

Remember, this is an emergency.

by Jim Scarantino | Mar 16, 2025 | General

From being a proactive, bold step to address the affordable housing crisis… to “waiting for the stars to align,” the once-vaunted Evans Vista Project has been left in the hands of astrologers.

Millions of dollars have been spent to acquire property and prepare and approve a Final Master Plan for the development we have been told would add 300-400 housing units. But at City Manager John Mauro and Mayor David Faber’s March 5 State of the City address, there was not a single mention of Evans Vista. That is, not until some members of the audience asked about it.

When confronted, Faber tried to dodge any responsibility for the failure of the project.

Evans Vista was supposed to be the city’s grand assault on the affordable housing crisis. In 2021, the city with state funding purchased 14.4 acres at the city’s entrance by the first traffic circle. As reported here, what started as an attempt to create much needed low-cost housing morphed into a grandiose master plan approved by city council to develop a village of multi-story apartment buildings, townhomes, retail shops and other structures, complete with a daycare center, dog park, amphitheater and other amenities. Economists hired by the city to judge the feasibility of the plan told the council it was simply too expensive to build.

I am in the process of writing up an alternative approach in which the city would completely ditch their absurd fantasy and get real about what can be done with what is probably the most undesirable plot of land within city limits.

In the meantime, Mayor Faber has put out several falsehoods about why the project is all but dead. This article addresses his dissembling.

State of the City Address

The annual State of the City address was billed as a review of “2024 Successes… Challenges & Lessons Learned… Aspirations for 2025.” The presentation was delivered in the Port of Port Townsend’s Point Hudson Pavilion, with the first hour broadcast by KPTZ.

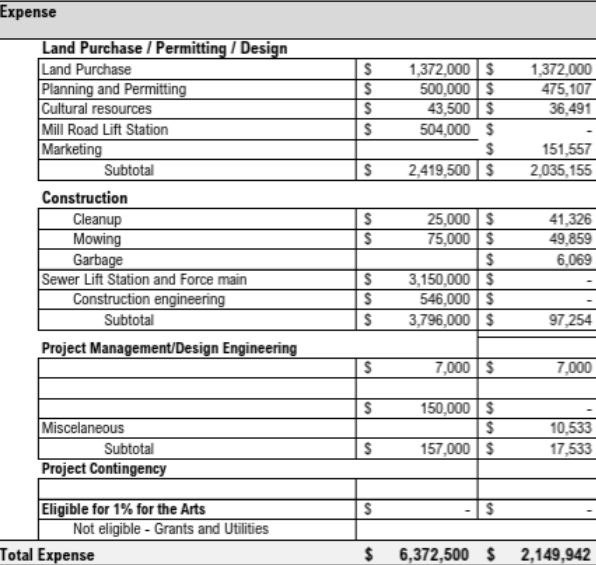

Despite an anticipated $6.37 million outlay as itemized in the city’s 2025 budget ($2.15 million spent to date), the stalled-out Evans Vista Project was not mentioned once in the 37 pages of State of the City materials.

One slide declared: “Housing is a basic need and it has risen to the top as one of the most pressing issues our community is facing.” [city’s emphasis] Yet not one photograph among the scores displayed showed either the current state of the Evans Vista property or any future vision for the 14.4 acres the city took off tax rolls to build its affordable village of the future.

City Manager Mauro led the presentation with a list of “major highlights” for 2024. Unsurprisingly the Evans Vista Project was not among the highlights. However it was also not included among the challenges facing the city, or among the “lessons learned.” It was not addressed at all until after Mauro’s presentation when Faber and Mauro fielded questions from the audience.

“Waiting For the Stars to Align”

Following Mauro’s prepared address, a couple of people asked about Evans Vista. Faber had to admit:

“We can’t actually get it built right now because we can’t afford it and developers won’t build it because you’d have to charge sky-high rents to make it actually pencil.” [Editor’s note: meaning, make it economically feasible]

Faber blamed lack of actual progress on the ground (as opposed to drawing pretty pictures) solely on interest rates. He said that when the city got started in 2021, the interest rate environment was very favorable. Indeed, it was about 0%. But now, as anyone who had passed Econ 101 would have expected, interest rates are much higher. Going back to the city council meeting when it voted to acquire Evans Vista and take on the project, not one second whatsoever was spent discussing the impact of interest rates on the project’s likelihood of success.

Did Faber and the rest of city council really believe that interest rates would stay at zero for years to come? Did they really base their decision to launch the city into what then-Mayor Michelle Sandoval predicted would be “an incredibly expensive” project based on such economic naivete?

Maybe. Let’s not forget this was the same city council, on which Mayor Faber and current Deputy Mayor Amy Howard served, that got the city deeply in debt to build the fiasco formerly known as the Cherry Street Project. This is also the city council that, with only one exception, voted to approve the mega-bucks Taj Mahal aquatic center to replace the Mountain View pool, another fantasy that never stood a chance of being built.

There was absolutely no consideration given by city council to economics when it jumped into the Evans Vista Project. None whatsoever beyond Sandoval’s dire prediction that it would be “incredibly expensive.”

Faber now says the city is “waiting” for interest rates to decline, and that they are “waiting for the stars to align.” He suggested the problem lies with the federal government, where things are, as he said, “spicy.”

Evans Vista has fallen far from what Faber lauded as a “proactive” effort by the city to create affordable housing. It has become a long-term, drawn out morass… at the mercy of the stars.

The Half-Million Dollar “Concept”

Another attendee asked about our recent report on city council spending half a million dollars soliciting and adopting a Final Master Plan that can’t be built. The questioner asked whether we had accurately reported what council paid for and approved.

Faber then lied.

He told the live and radio audiences that while he had not read our report, there was in it “something about a claim that the plan adopted by city council was a final plan. In fact, it was a conceptual plan.”

They paid $500,000 for a concept?

The record speaks for itself.

Table of budget and expenses for Evans Vista Project, from the city’s 2025 final budget. Right-hand column are expenditures to date.

As my recent article reported, in August 2022, Jefferson County gave the city $500,000 of federal COVID money to fund “the Evans Vista Master Plan.” The city then put out a request for architects. Interested architects were informed that:

“the project is to develop a master plan and land use entitlement applications [e.g. plats] to develop Evans Vista into an affordable workforce housing development.”

On November 7, 2022, the city approved a contract with Thomas Architecture Studios (TAS) to develop that master plan. On November 20, 2023, the action item under “New Business–D” on council’s agenda was “move to approve Exhibit A, the final site design for the Evans Vista Master Plan so the Project Team can apply for subdivision entitlements.” [emphasis mine]

Exhibit A showed the overall layout of the final site plan:

Evans Vista Master Plan adopted by city council

After the architect presented the site plan, the economists told city council that the design was too expensive to build. Construction costs would start at $111 to $126 million. Those were 2023 dollars. The cost today would be higher due to inflation.

Much higher rents would have to be charged than currently prevail in Port Townsend’s already unaffordable rental market. Interest rates would have to drop significantly and the economy would have to return to conditions resembling those in 2013. And construction costs would also have to be reduced significantly, which was not possible if the kinds of buildings in the Final Master Plan were used.

After hearing that the plan was economically unfeasible, city council nonetheless unanimously approved this Final Master Plan for Evans Vista.

My article also reported that the city has not moved forward with platting the project based on the Final Master Plan… because it is unfeasible and no builder will touch it. Instead, the city is pivoting and trying to interest developers in taking on smaller pieces, without being tied down in any way to the grandiose plan approved by city council. In other words, the $500,000 Final Master Plan adopted by council has in fact been demoted to a mere “concept” that is now being cast aside because it cannot be built.

Meth Meadows

What is the actual “State of the City” at Evans Vista? We have provided some photos.

The featured photo at top shows a sample of the garbage left behind nightly by transients taking up residence at what would be the entrance to the proposed development. The city has provided a dumpster to encourage transients to be tidy. I have observed people going in the dumpster and coming out with the trash that soon again surrounds their camps.

The photos below show the growing transient camp on the city’s property near the DSHS building.

This camp, according to law enforcement sources, has become a violent place. Heavy methamphetamine use makes matters worse. While taking these photos a man emerged quickly from one of the tents and came straight at me quite aggressively. I got in my truck and drove off, watching him glare at me from my rear-view mirror.

We might want to call Evans Vista “Meth Meadows” to reflect the reality on the ground for the foreseeable future. In 2022, I had named the wooded part of Evans Vista “Port Townsend’s Fentanyl Forest,” as that was the drug of choice for its residents. But the city cleared them out. Now a sprawling camp of addicts has taken over the meadows on the northern part of the property.

Few Hard Facts, an Exercise in Political Theater

A lot of time and expense went into the preparation of the State of the City address. None of Faber’s predecessors staged such political theater. Nor did Mauro’s predecessor expend resources and staff time in producing such a show.

We got a lot of glib phrases and self-congratulatory sentiments. We got adjectives. We did not get data.

One key metric not reported by Mauro and Faber is the only meaningful measurement of progress against the affordable housing crisis declared to be an emergency by local governments in 2017. Though the mayor and city manager did not report that statistic, we can confidently give the precise number of affordable housing units added in response to the city’s costly forays into the housing market, from the Cherry Street Project to the Evans Vista Project. That number is zero. And it will remain zero, as Mayor Faber rationalized in an act of surrender, until “the stars align.”

Or we can search a different universe of possibilities. That will be the topic of my next article on the Evans Vista Project.

by Stephen Schumacher | Mar 11, 2025 | General

[Author’s 2025 update: The following article is a snapshot in time reporting what I learned and loved about the Port Townsend Food Co-op after a decade of intense involvement. It was originally published nationally in the 1994 Loompanics book catalog, but never appeared locally until now.

The concluding section makes clear how reality doesn’t always live up to ideals, noting the dual dangers that growing co-ops face of either imploding due to misguided idealism or getting “co-opted” into becoming a corporate supermarket clone. So it’s interesting looking at how today’s Co-op compares to this view forward from 30 years in the past.

This historical perspective might be especially timely as our Co-op has been targeted for half a year by a politically-motivated smear campaign, which amid personal attacks has also raised claims about management style, workplace safety, wage inequality, microaggressions, need for unionization, etc. These claims are hard to sort out given their weaponization by the ongoing pressure campaign.

Whatever legitimate issues remain may be illumined by this article’s exploration of the unique mission of food co-ops, what makes them special, and how ours has changed over the years, for better or worse. What qualities are vital for our Co-op to preserve, and is anything that’s been lost worth restoring?]

————————————

Do you know anything about food co-ops? I love food co-ops! Holdovers from the 60s and 70s, these hippie-born hangouts have grown up a bit over the years but still retain much of their savor. When I visit a new city I always try to check out the local co-ops.

Food co-ops are practical, too. They started from the practical reality that the pure, simple bulk foods the hippies wanted weren’t for sale anywhere on the market. So the hippies became grocers, and eventually business people, of sorts. Not because they wanted to be, but because they had to be, or go hungry for basic foods.

But because they were hippies and were idealistic, they didn’t set up run-of-the-mill capitalist businesses. They had ideals about cooperation and consensus and egalitarianism and lack of hierarchy and workplace democracy and not being focused on profits. Heads stuffed with ideals, they also valued hands-on work and invited as many people as possible to share the work of running the store.

Did I say work? More like productive play, when it comes down to you as a co-op member taking a break from the work-a-day world to bag raisins or run the register for a few hours a week as your friends and neighbors stream through. Sometimes you want to go where everybody knows your name, and they’re always glad you came … more like checking in at Cheers than punching in at the assembly line!

It’s also a bit like joining a fraternal society, because co-ops do their best to cooperate with other co-ops around the world. Though separate legally, most food co-ops welcome visiting members from other co-ops and let them shop at reduced member prices. Your home-away-from-home in your community extends to connect you to home bases throughout North America and the world.

The Big News

So that’s the big news: the 60s aren’t dead, for co-ops are still alive and they’re even growing. Their doors are open and you can come in and get great food and save money and have fun and maybe even get involved in something radical!

I’m going to go into some more detail about the points I’ve breezed through above. I’ve been ardently involved with co-ops heavily for the past decade, and I’m still trying to figure out what it is about them that so attracts me. The word “cooperative” is awfully vague — at their core, what exactly are food co-ops?

It’s the Food!

First of all, there’s what food co-ops sell, which is food. Not just any kind of food, but high-quality, lightly-processed, low-pesticide, nutritious food. ”Natural” food. Most of this food isn’t exotic — it’s just the kind of basic food your grandparents enjoyed. Back in those days, before DDT, preservatives, bovine growth hormones, chlorination, fluoridation, irradiation, etc., etc., nobody made a big deal about natural, whole, unadulterated food, because that’s all there was.

There was also a lot less chronic disease; for instance, heart attacks and clogged arteries were rare until the turn of the century. Cancer rates remain much lower in countries with less meat and more fiber in their diets. The low-fat, low-salt, low-sugar, low-processing, low-poison food for sale in food co-ops is the model of good nutrition.

Co-ops Are Selective

It’s true, you can’t find everything in a co-op. Coca Cola pretends to “add life” and be “the real thing,” but since these claims are hogwash, co-ops don’t carry Coke. Co-ops have product selection guidelines, supplying goods that are whole, organic, fresh, local, low-cost, earth-friendly, politically-correct, and/or hard to find. Glop like Coke doesn’t make the grade.

But that doesn’t mean co-ops sell only brown rice and tofu! It’s amazing the variety of natural foods available nowadays, many of them healthier alternatives for standard American favorites. Natural sodas, turkey dogs, veggie burgers, wheat-meat sausages, soy-cheese pizzas, etc. make upgrading one’s diet pretty painless

You can also get cookies, chips, frozen dinners, bagels, ice cream, corn flakes, and most other popular foods at co-ops. The difference is in the ingredients: whole-wheat flour, low or no salt, or maybe fruit-juice sweetening instead of refined sugar. They’re more nutritious than the famous name brands and usually taste at least as good.

Of course, no matter how many times the word “natural” appears on the label, I doubt the nutritional value of most of the sweets and frozen treats co-ops carry. Members (and their kids) want these sweets, and they’re better than the standard “unnatural” versions, so co-ops provide them. Sometimes I hear members say things like, “If the co-op carries it, it must be OK,” as they stock up on natural junk food!

Be Smart – Bulk Up

Quaker Oats sells for about two and a half bucks for 18 ounces of rolled oats. I’m used to paying $.49/pound for organically-grown oats at my co-op, which also sells non-organic oats as good as Quaker’s for $.25/pound. It’s amazing how much money consumers waste paying for packaging, advertising, shelf-space kickbacks, and corporate profits.

You can save a lot of money buying cereal, flour, rice, nuts, beans, chips, oil, mustard, maple syrup, pasta, herbs, salsa, honey, raisins, olives, dog food, soap, etc., etc. out of bulk bins at food co-ops. All that’s missing is mountains of landfill-bound packaging, the brand name, and most of the price.

Bulk is the smart way to shop. You can buy as much or as little as you want, so you can sample without committing to a boxful. You’re getting whole foods without the frills. And you can save even more money at co-ops by placing bulk orders in advance — just be sure you like wild rice before you order 25 pounds of it!

Only at Co-ops

There’s an entire world of products you can’t find in supermarkets, only in food co-ops and other natural foods stores: organically grown produce, exotic cheeses, therapeutic herbs, sea vegetables, macrobiotic foods, special diet supplements, natural body care products, and the list goes on.

Organic produce is grown without synthetic fertilizers or pesticides using sustainable agriculture which builds up rather than depletes the soil. Farm workers aren’t being poisoned in the growing, and you won’t be poisoned in the eating. Richer soil can also mean more minerals in your produce, as well as better taste.

Many co-ops cultivate relations with local farmers so they can offer produce that’s extra fresh. Vegetables like broccoli are sometimes trucked from coast to coast before they appear on supermarket shelves, wasting both fuel and nutrition. It’s better to have a strong sustainable agriculture base in one’s community.

Be Your Own Doctor

A real showpiece of my co-op is our great herb section. We have hundreds of hard-to-find botanicals alphabetically arranged in air-tight bottles. Prices like $17.06/pound may seem forbidding, until you get to the counter and find your pouch of fluffy powder costs only 23 cents!

Many knowledgeable people prefer to treat themselves with time-tested herbs, which are usually gentler and less expensive than the latest patent drugs from the chemical/vivisection/medical fraternity. Few have ever been harmed by misusing herbs, while untold thousands die each year from the side effects of FDA-approved drugs (even aspirin kills hundreds a year).

Nevertheless, the FDA is continually trying to get the power to classify traditional herbs as drugs or “untested food additives,” in order to get them off the market or into the exclusive control of “approved” multinational corporations. Who benefits? Certainly not the consumer. The extensive herb sections in food co-ops are treasure troves of self-care options.

The Same Old Story

It’s hilarious and sobering checking out an old book like Omar Garrison’s The Dictocrats from 1970 to see how off-base the FDA has been through the years. During the ’60s the FDA seized yeast and honey off the shelves of health food stores — the agency preferred sugar and cyclamates.

They derided as false advertising and prosecuted discussions of the connection between dietary fat and heart disease, or between Vitamin C and healing. The FDA banned books on alternative medicine (literally burned Wilhelm Reich’s) under the pretext of being “an extension of the label” of unidentified food supplements.

With the perspective of years we can see that the FDA was on the wrong side of almost every one of its disputes with the health food industry. What was persecuted as “food faddism” is now reported as fact by Time magazine. The lighter, fresher diet advanced by old-time “health nuts” is now the common wisdom, while the heavy, fatty, sugary slop the FDA promoted is only defended anymore by vested interests like the beef industry.

More Monopoly Medicine

Unchastened, the FDA is at it again with another assault. Calcium’s role in preventing osteoporosis is the only supplement health claim the FDA presently accepts, and it’s trying to ban everything else, the first amendment be damned. The FDA is threatening to keep stores from selling therapeutic herbs, amino acids, bee products, and all vitamins and minerals more nutritious than the Recommended Daily Allowances!

The health food industry and its customers are not rolling over and playing dead — instead, Congress received more letters in 1992 demanding health freedom than about any other issue besides the economy. The result was a one-year moratorium on the FDA’s oppressive new regulations.

A year later, on Friday, August 13, 1993, my co-op draped itself black as part of a nationwide Blackout Day, a wake-up call to political action. Threatened products were marked with black dots for the duration to warn customers these products may disappear if the FDA isn’t stopped. Action booths were set up with full information and pre-addressed postcards to encourage grass-roots support for passing protective Dietary Supplement Health and Education Acts (S. 784 in the Senate and H.R. 1709 in the House).

As of this writing, the outcome is still in doubt. This is a crucial fight, for the FDA’s new rules are a prescription for disaster. The health care crisis in this country is caused by monopoly medicine and won’t be solved by more of it!

The Co-op Difference

Most everything said above applies equally to privately-owned natural food stores and to co-ops. They carry the same great products and are equally protective of your right to make your own health choices. Some natural food stores look almost indistinguishable from co-ops.

But there are differences, mainly of culture and orientation. Food co-ops came out of the hippie culture, so their staples are back-to-basics natural foods like fresh fruits and vegetables along with bulk grains, beans, nuts, and herbs. Private stores tend to emphasize “nutritious” over “natural,” with shelves full of megavitamins, pump-you-up bodybuilding supplements, and alternative health books.

Co-ops have a special kind of internal structure, neither socialist nor capitalist, that was pioneered in 1844 by a 28-member weavers’ co-op in Rochdale, England. “Capital is necessary for any enterprise, but while capitalists rent labor and earn profits, cooperatives rent capital and the members earn profits through their participation” (Kaswan, Whole Earth Review, Spring 1989). Important co-op decisions are made by members actively involved in and affected by co-op operations, not by investors or speculators.

Each co-op is organized to fulfill a specific need of its voluntary members, so it has a mission in life beyond the standard corporate imperatives to maximize growth, profits, and executive pay. Because a food co-op is a consumer cooperative, its owner/members are food consumers. Providing them with the best deal on the best whole foods is a food co-op’s bottom line.

The International Co-op Conspiracy

100,000,000 Americans are members of over 45,000 cooperatives, including credit union, group health care, agriculture, rural electric, housing, insurance, and worker co-ops. When the state capitalist economy leaves some people out in the cold, when consumerism built on invented demand doesn’t supply everyone’s desires, mutual-aid co-ops can be a satisfying solution.

In Central America, India, Indonesia, Eastern Europe, and around the world, co-ops are one of the few means available for people to help themselves out of oppressive circumstances. The outstanding example is the Mondragon system of cooperatives tucked away in the Basque region of northwestern Spain — probably the most successful social experiment in the history of the planet!

The Mondragon Miracle

Can you believe it? Founded in 1956 by the passionate Padre Arizmendi after 15 years of solitary spadework, his 5 member stove co-op has grown into a multi-billion-dollar network of 173 cooperatives employing 20,000 people. Mondragon co-ops include Spain’s fastest growing bank, hundreds of K-Mart style consumer stores, health care, insurance companies, pension management, entrepreneur development, robotics research, heavy equipment manufacture, and just about everything else under the sun.

And all this was accomplished through a sophisticated, self-adjusting system emphasizing workplace democracy, ownership gained by participation, self-financing from the local co-op bank, continuous cultivation of new co-ops, and a cultural commitment to solidarity: *all acts must, at the same time, benefit and respect the needs and concerns of everyone affected — individuals, their cooperative, other cooperatives in the system, and the larger community” (Jaques and Ruth Kaswan, “The Mondragon Cooperatives,” Whole Earth Review, Spring 1989, pp. 8-17).

A central co-op principle is cooperation among co-ops; Mondragon does it in spades! No other co-ops have ever come close to its interlocking, diversified system, but all cooperatives aspire to this ideal and have a conscious commitment to mutual support. Taken together the world’s co-ops are a global conspiracy — an open conspiracy with 700 million members at large.

The Great Good Place

Getting back to home. I’ve got to admit that such world-girdling considerations are only a very small part of why I love co-ops. Mostly it’s the day-to-day joy I experience walking into my own local co-op and immersing myself into its soul-soothing ambiance.

Today my fingers played over the keys of a musical cash register while I enjoyed the vista of chatting member-workers bustling backstock to the retail shelves amidst chatting member-shoppers carelessly selecting groceries. The business at hand seemed to be conversation first, food second. One shopper confided to me, “I have to come here to get some social interaction. I work at home and don’t even get to talk to people. I come to the Co-op to catch up.”

Ray Oldenburg’s book The Great Good Place rhapsodizes about “third places [that] exist on neutral ground and serve to level their guests to a condition of social equality [that’s] remarkably similar to a good home in the psychological comfort and support that it extends. … a source of news along with the opportunity to question, protest, sound out, supplement, and form opinion locally and collectively. …

“The activity that goes on in third places is largely unplanned, unscheduled, unorganized, and unstructured. Here, however, is the charm. It is just these deviations from the middle-class penchant for organization that give the third place much of its character and allure and that allow it to offer a radical departure from the routines of home and work.”

Co-ops are great good places. They are Temporary Autonomous Zones. They are community crossroads, counterculture cynosures, neighborhood news services. They are R & R for overworked psyches, refuges from dog-eat-dog reality, and perhaps the seeds of deeper and more sustaining realities.

The Abolition of Work

Food co-ops have this feel of the “third place,” while trying to integrate it with the business of providing good food and service. At their best, they seem like real-world exercises of the vision that Bob Black broadcasts in his essay, “The Abolition of Work“:

“A ‘job’ that might engage the energies of some people, for a reasonably limited time, for the fun of it, is just a burden on those who have to do it for forty hours a week with no say in how it should be done, for the profit of owners who contribute nothing to the project, and with no opportunity for sharing tasks or spreading the work among those who actually have to do it. …

“Such is ‘work’. Play is just the opposite. Play is always voluntary. What might otherwise be play is work if it’s forced. …The player gets something out of playing; that’s why he plays. But the core reward is the experience of the activity itself …some things that are unsatisfying if done by yourself or in unpleasant surroundings or at the orders of an overlord are enjoyable, at least for a while, if these circumstances are changed.”

Much of the work at many co-ops is done by members part-time in exchange for food discounts or other benefits — not as a requirement of membership but as a welcome option that satisfies Black’s standards for play. In a convivial, ego-free environment, professionals and working stiffs and assorted unemployables can break up their lives with some hands-on cheese cutting or clerking or cleaning — as one CPA/discount worker remarked, “I can do anything for 4 hours a week!”

Whither Food Co-ops?

I have been describing the ideal situation; co-ops often find themselves stretched between apparently opposite commitments to cooperative purism and efficient operations. The Consumers Cooperative of Berkeley, at one time America’s largest food co-op with 12 stores and 100,000 members and $83.6 million in annual sales, failed in 1988 partly due to this conflict. The board factionalized into progressive versus economic camps, the staff collected inflated paychecks while co-op assets were sold off, and the membership defected in dismay over infighting and the disappearance of politically-taboo products from the shelves.

Berkeley is an extreme case, and remember that for 50 years it was a pioneering and successful co-op. Did cooperativism fail at Berkeley, or is this an example of what can happen when co-ops neglect their underlying principles? Many employees hadn’t been educated about co-ops, didn’t bother to become members, and felt alienated from their co-op bosses. A weak board literally gave away the store in contract negotiations, putting reflexive sympathy for union causes ahead of the membership’s interests (source: “What Happened to the Berkeley Co-op?”, excerpted in Cooperative Grocer, January, 1992).

As food co-ops grow and find themselves directly competing with huge corporate supermarket chains, they start discovering every incentive to become more like supermarkets and less like co-ops. Member involvement in store operations gets phased out, replacing the energy of enthusiastic part-timers with the professionalism of stressed-out staff. Whether at McDonald’s or Mondragon, full-time service work within a power structure can be a stupefying experience that makes cooperative ideals seem pretty hollow. When a co-op looks like Safeway and works like Safeway, why should its shoppers and workers care that it isn’t Safeway?

One answer is that supermarket co-ops remain excellent natural food stores with top-quality products and a benign corporate outlook which plows profits back into the co-op and its community. But those who prefer small-fry co-ops do feel that something intangible gets lost as co-ops grow into increased hierarchy and organization. As a co-op gets less fun to work in, it gets less fun to shop in and less like a great good place to hang out in. Play time is over — it’s back to work. Where’s the co-op difference?

Original article sources from 1994

I hope that food co-ops will someday crack the nut of how to grow without losing what makes them great. I wonder whether co-ops will prove to be just the wave of the past, or whether the Mondragon model will eventually take over the earth. What I do know is that right now many magic co-ops survive and thrive for you to enjoy — there may be one in your home town. Check it out!

————————————

Illustrations by Barbara Williams and Shaun Hayes-Holgate

by Jim Scarantino | Mar 7, 2025 | General

How is Port Townsend doing financially? City Manager John Mauro tells us pretty much all is well.

Here he is in his City Manager’s preface to the city’s 2025 budget:

“If you take the time to review the previous years’ budgets – or even just the budget messages from me – you’ll see them evolve into something increasingly clear-eyed, strategic, and honest. This year we attempt to keep moving forward in a similar fashion, with a balanced, smart, and forward-thinking budget that reflects our community’s values and sets us up for enduring success.”

In an email exchange with the Leader, he deflected concern about the city’s budget actually being a deficit budget (keep reading). He insisted the city’s budget was instead “a structurally balanced budget.” That phrase does mean something. Indeed, a structurally balanced budget is a good thing. The Government Finance Officers Association provides this explanation:

Most state and local governments are subject to a requirement to pass a balanced budget. However, a budget that may fit the statutory definition of a “balanced budget” may not, in fact, be financially sustainable. For example, a budget that is balanced by such standards could include the use of non-recurring resources, such as asset sales or reserves, to fund ongoing expenditures, and thus not be in structural balance. A true structurally balanced budget is one that supports financial sustainability for multiple years into the future. A government needs to make sure that it is aware of the distinction between satisfying the statutory definition and achieving a true structurally balanced budget.

So is Port Townsend’s 2025 budget a structurally balanced budget? Should we not be concerned about the fact that the city’s budget is only balanced by spending reserves? Is the city being set up for success, as Mr. Mauro tells it, or something else?

The “Fiscal Cliff”

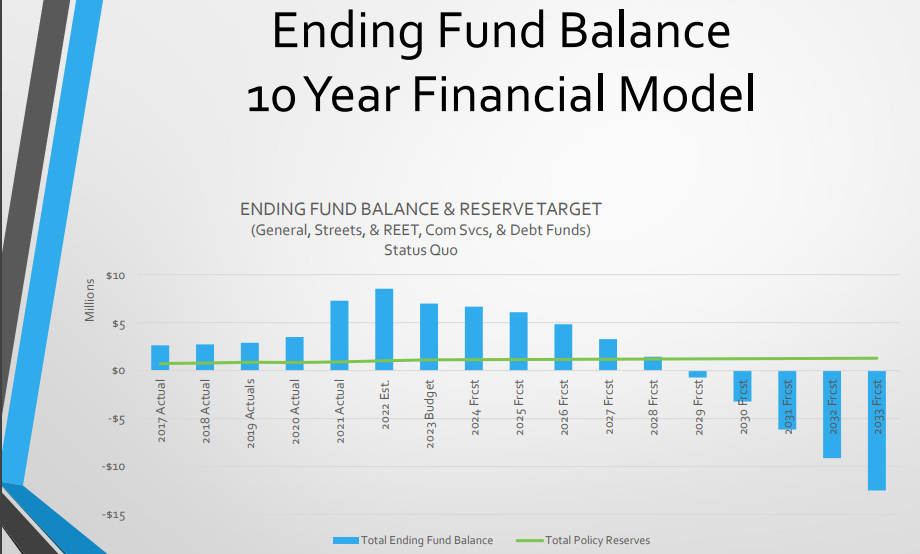

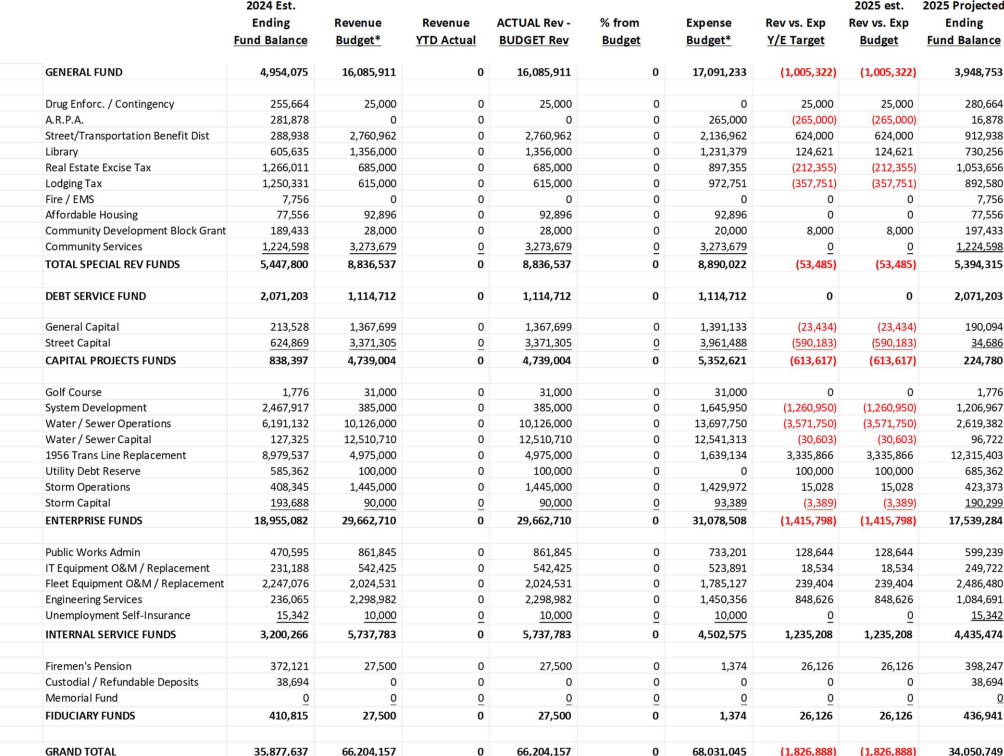

At the end of 2023, I wrote an article entitled, “Port Townsend is in Trouble.” It copied the graph featured at the top of this article directly from the report of the city’s Sustainability Task Force (on which I have also reported).

That graphic shows the city heading over a “fiscal cliff,” to use the words of the Sustainability Task Force, and certainly does not reflect a structurally balanced budget that delivers sustainability. To stave off that deep dive, the city has been doing some quite smart things, such as paying down debt and setting aside funds for future debt payments.

The 2025 budget shows just over $2 million being banked for paying debt coming due next year. Likewise, funding for streets is up significantly from taxing through the Transportation Benefit District, and the budget shows large expenditures on capital projects needing attention. Further, a rainy day fund had about $248,000 at the start of the year, not a huge amount, but at least something positive.

On the other hand, both the general capital and street capital funds show large deficits. Expenditures of almost $4 million on streets will leave less than $35,000 in that account by year end. Expenditures of almost $1.4 million from the general capital budget will pull that account into the red and leave under $200,000 by year’s end. That leaves very little for next year’s needs.

Despite some accounts doing well, there is a lot of red ink, spending in excess of income, throughout the city’s budget. The result is an overall deficit of $1,826,888.

Some kinds of municipal expenses can benefit from federal and state grants, and money from such sources is funding a good deal of Port Townsend’s infrastructure work. The general fund that pays for City Hall’s operations and staffing is another matter.

Burning General Fund Reserves

There is no more federal COVID money, aka American Rescue Plan Act funds, to supplement Port Townsend’s general fund. The city booked about $2.755 million in COVID funds in 2022. The city’s general fund peaked that year at almost $7 million (see the graph heading this article). The COVID money is now gone. These emergency funds were supposed to be spent on public health, infrastructure, supporting local businesses impacted by government-mandated shutdowns and supporting “essential” workers.

These federal funds bought two police vehicles ($356,000), contract legal services ($300,000), a roof repair for the pool ($91,500) and a Bobcat excavator and mini-excavator ($98,725). More questionable expenditures show in the city’s final reporting on how it used these one-time emergency funds: remodeling City Hall ($546,000), an “engagement survey” ($50,000), expanding payroll by adding a “Long Range Planner” ($240,000) and various outlays (about $500,000) in salaries and consultants for the failed golf-course revisioning as Central Park and the megabucks Taj Mahal aquatic center proposal.

With ARPA funds now showing a zero balance, 2025 will mark the third straight year of overspending out of the general fund. At the same time, the cost of City Hall salaries and operations has increased. Some line items have more than doubled.

By the end of this year, the general fund reserve will have been drawn down almost 43% from its 2022 level. From almost $7 million in 2022, general fund reserves will be reduced to less than $4 million by year’s end.

In 2025, the city is projected to pull about another $1 million from its general fund reserves to compensate for general fund deficit spending. There is no reason to believe that on the current trajectory this account won’t be pulled down further in coming years.

Spending on the Mayor and Council grew from $122,362 in 2022 to $291,434 last year, but has been cut back to $237,581 for 2025, still a 94% increase over 2022. The City Attorney account grew from $483,504 in 2022 to $826,288 last year, a 71% increase. Some money has been shaved off the City Attorney budget for 2025, coming in at $762,723, still a huge increase since 2022.

Many other City Hall line items have also grown significantly since 2022:

- Communications, from $0 to $187,736

- Human Resources, from $340,690 to $495,865

- Planning & Development, from $1,108,492 to $2,140,316 ($2,510,257 in 2024)

- Finance, more than doubling, from $465,764 to $1,055,130

- Police Administration, more than doubling, from $552,993 to $1,219,402

- Police Operations, from $2,791,357 to $3,753,359

Even in the face of persistent deficits, the city continues to expand payroll.

It will be hiring three seasonal workers in 2025 for streets, parks, storm and waste water, and water distribution tasks. It is also adding four full-time positions: water maintenance worker, park maintenance worker, community services director and arts and culture coordinator.

Washington’s rising minimum wage will drive up labor costs for seasonal works and entry level library workers. It pushes higher all the wages above it by increasing the base wages on which the rest of the pay scale is built, called “wage compression.” Further, as the Leader has been reporting, raises will be coming to City Hall that are not in the 2025 budget, adding to the red ink already requiring spending reserves to create a “balanced” budget.

Worrying Signs

To avoid falling off the fast-approaching fiscal cliff, substantial real growth in the city’s economy is required. That was the message from City Engineer Steve King back in 2023. He was refreshingly frank about the approaching crisis. “Our tax structure absolutely requires growth,” he said. To avoid crisis, a “radical” change is needed to achieve a high rate of growth not seen in recent memory.

So how is the city’s real economy doing in providing the growth required by our tax structure?

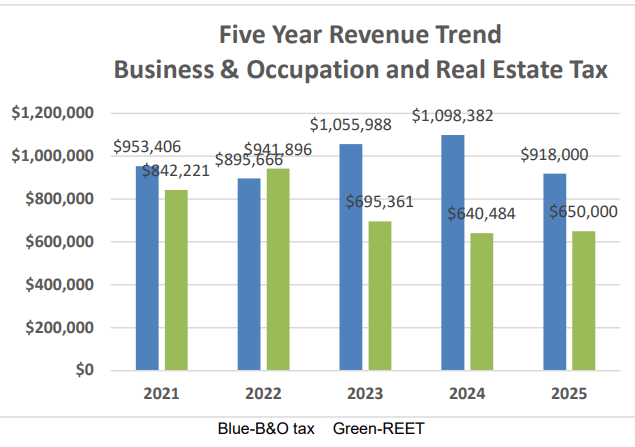

The retail sales tax brought in an estimated $3,397,900 in 2024. This is up from not only pandemic years, but also higher than 2018, when the city netted $2,529,757. That may look like a much better year, except one must adjust for inflation. The 2018 revenue, adjusted for inflation, would be worth just under $3.2 million today. That means the city’s retail and other sectors that pay the retail sales tax have barely expanded in seven years. That is stagnation.

Property values, though, are not stagnating. Owners can expect to be paying more, with some of that increase heading towards the city’s accounts. The city can also increase the tax by the permitted 1% annual bump (count on it).

But the stagnation in the underlying economy can’t be ignored. Revenue from the Business and Occupation and Real Estate Excise Taxes are actually predicted to decline in 2025.

Port Townsend’s tourism economy is not experiencing any real growth. Lodging tax revenue is a fairly good barometer of how robust the tourist economy is. 2024 saw $528,096 in lodging tax revenue. That is below pre-pandemic 2018 when lodging tax revenue was $551,080. Adjusting that figure for inflation, in today’s dollars the 2018 lodging tax revenue would be $638,597. This means that in real terms the city’s tourism industry has shrunk considerably. Troubles at Fort Worden, a major driver of local tourism, does not mean good news for the city’s future lodging tax revenues.

And the costs of running a city continue to rise. Inflation is hanging around, not dropping as much as had been anticipated a couple years ago.

Structurally Balanced? Nope.

The question is not whether the city’s 2025 budget manages to balance out on paper. The question is whether the city’s budget, judged by the standards articulated by the Government Finance Officers Association in defining a “structurally balanced” budget, “supports financial sustainability for multiple years.”

A budget that uses reserves to cover ongoing expenditures, by definition, does not meet that criteria. The city’s 2025 budget, as in the preceding two years, uses reserves to cover ongoing expenditures. It is, therefore, not “structurally balanced” as Mr. Mauro claims. It continues on course over the financial cliff predicted by the city’s Financial Sustainability Task Force.

Mauro, as in his recent comments to the Leader about the city’s deficits, assures taxpayers not to worry about the red ink. “It’s not a coincidence.” he wrote in an email to the Leader, “that we won a national [International City/County Management] award for the work done by community members, staff, and Council – and something that should provide some assurance to our community that the City, through City Council action on budgets and related policy, is making sound financial decisions over multiple years.”

That award (self-nominated, by the way) was for work showing the city falling off a fiscal cliff three years from now. It was not an award for continued payroll expansion and deficit spending that will confirm that grim prediction.

by Jim Scarantino | Mar 2, 2025 | General

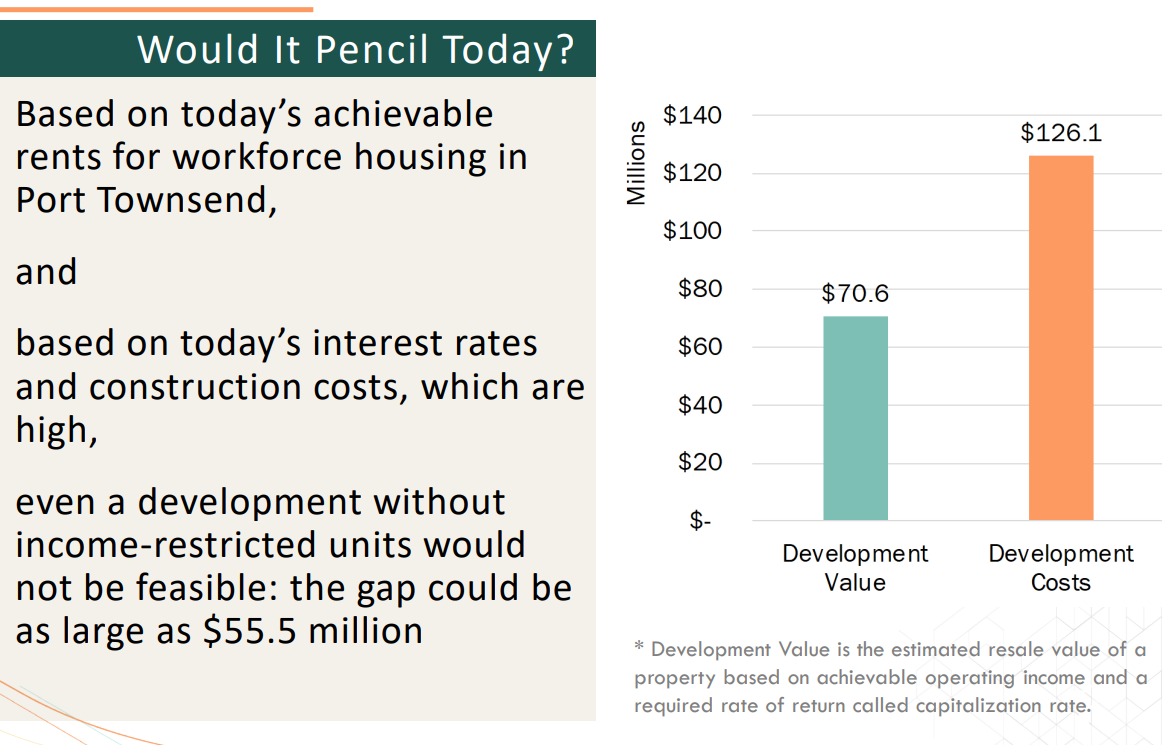

The City of Port Townsend paid architects almost $500,000 to draw up a plan for Evans Vista that is too costly to build. The city purchased the 14.4 acre Evans Vista property in 2021 to address the city’s affordable housing crisis. The architect’s pictures, like the rendering above, are very nice. But the bottom line is that all that money produced a project that can’t be built.

Total costs would start at $111-126 million (2023 dollars) and go up from there. The economic analysis performed only after the drawings were done shows that the market value of the Evans Vista Project would be $55.1 million below the costs of development.

Despite being confronted with a pro forma showing the project was not economically feasible, the Port Townsend City Council on November 20, 2023, voted to approve the plan so that it could move forward. Since then, nothing much has happened on the ground. There is no contractor, no investor pouring tens of millions of dollars into building a costly, hip neighborhood by the pulp mill in the middle of large homeless camps.

As things stand, the Evans Project is a failure. Over $2.1 million has been spent thus far. The project was supposed to address the immediate and crushing shortage of affordable housing in our community. More than three years have passed and not a single unit of affordable housing has been added.

I asked the city when we could expect to see the first affordable housing available at Evans Vista. City Engineer Steve King provided this answer: “These projects by their very nature move slowly as we expected…” There are many excuses for the project moving slowly, everything from holding back until a sewer lift station is built to the more intractable problem of finding a private developer who will risk their money on a seriously losing proposition.

But this was not supposed to be a long, drawn-out morass. Nobody told city council up front this project would stall out. It was supposed to be a fix for the city’s crushing shortage of affordable housing… yesterday, today, tomorrow, not untold years in the future, if ever.

We’ve seen this before: the debacle of the Cherry Street Project, the “revisioning” of the golf course as a Central Park, and plans for a Taj Mahal aquatic center to replace the Mountain View pool. Millions of taxpayer dollars have been spent on lots of drawings, scores of meetings and listening sessions, and thick books of reports, with little else to show for it.

An “Incredibly Expensive” Idea

On December 6, 2021, city council voted to purchase the 14.4 acre Evans Vista property, located east of the highway before the first traffic circle upon entering town. $1.3 million from the Washington Department of Commerce paid for the land, on the condition that at least 25% of housing units in any future development would be “affordable.”

The Evans Vista property is outlined in red.

These acres had long been the place of last resort for addicts who lived in appalling conditions among the trees. I covered that story in my article on what was then being called Port Townsend’s fentanyl forest. During the term of the late former Mayor Brent Shirley an effort to add about 200 housing units in that area had made some progress until the developer determined the project was not feasible due to the location.

As explained by City Engineer Steve King, the new plan was to create at least 100 affordable housing units. He said that number of residences could be served by the water and sewer infrastructure already in place. The “due diligence” conducted before purchase looked for signs of Indian use (none found at the cost of $36,491) and reviewed zoning codes. No economic feasibility analysis of any kind was conducted.

City council and staff quickly leaped from focusing on affordable housing to imagining an entirely new neighborhood with a mix of affordable and market-rate housing, complete with a central plaza and various amenities. Then Mayor Michelle Sandoval predicted it would be an “incredibly expensive” project.

Cherry Street Project demolition

Current Mayor David Faber, Deputy Mayor at the time, said, “I am nervous” about “again'” getting “the city significantly involved in a project that doesn’t necessarily have a clear end project yet — given the status of the Cherry Street Project and so forth.” He did not want another “long-term, dragged-out morass.”

The Cherry Street Project, as most readers know, was the city’s failed effort at creating affordable housing by purchasing in 2017 and barging from Victoria, B.C. a 60-year old 4-unit apartment building and moving it to city-owned land on a hillside above the golf course. The cost of the project was never determined up front and continued to explode. The building sat empty, a vandalized eyesore. Eventually, the city gave up and tore the building down in late 2023. The land sits empty and has not been sold. Taxpayers are still paying off the debt incurred to rehabilitate the building and grounds.

Though he did not want another “long-term, dragged-out morass,” Faber stated quite clearly regarding the embarrassment of the failed Cherry Street Project, “I wouldn’t change a single thing about what we did.” Sadly, the Evans Vista Project has played out along similar lines that led to the failure of the Cherry Street Project.

Ignoring Hard Numbers

In early 2018 it became apparent that much more money would be needed for the Cherry Street Project. The initial hopes of quickly adding affordable housing in the Fall of 2017 for a couple hundred grand had evaporated. This would be a much more involved, more time-consuming and more expensive project, i.e., “a long-term, dragged-out morass.”

City council voted to approve a bond that saddled taxpayers with debt and interest of about $1.4 million. Before the vote, council was informed of a pessimistic pro forma, an economic projection and analysis, showing the project defaulting within two years. City council, which then included Faber and current Deputy Mayor Amy Howard, voted to issue the bond anyway. As council had been forewarned, the project cratered. Taxpayers got burned and years of effort were wasted without adding a single unit of affordable housing.

Fast forward to 2021, when the city acquired the Evans Vista property. The city obtained $3.1 million from the state to help with acquisition and infrastructure costs. In August 2022 the county gave $500,000 of Federal COVID money to fund “the Evans Vista Master Plan.” A couple months later the city issued a “request for qualifications” from architects who could prepare a master plan and applications for land use permits for “an affordable and mixed-use housing development.”

Time was of the essence:

“The development of a mix of 100-150 workforce housing units is meant to deliver urgently-needed supply and to activate the Evans Vista neighborhood as part of the area’s emerging commercial and business environment.” (Emphasis added.)

On November 7, 2022, city council approved a $500,000 contract with Thomas Architecture Studios (TAS) of Olympia. City Councilor Ben Thomas abstained on grounds he lacked enough information to vote on such a large contract.

A year later, November 20, 2023, city council approved the “final master plan design.” The project had grown to 319 units with multi-story apartments — walk-ups and “podiums” with parking under the building. There would be 16 townhomes, 8,500 square feet of retail space, a 2,000 square-foot daycare center and 3,000 square feet of other structures, such as pavilions and meeting spaces. Only nine acres of the 14.4 acres would be developed due to the steep slopes and preservation of a wetland area. The entirely new neighborhood would come with plazas, a dog park, an auditorium and stage, a “madrona picnic grove” and multiple “art plinths.”

City Manager John Mauro said he was “very excited” about the TAS design.

An air of unreality reigned. City Planning Director Emma Bolin penned a fanciful Google review from May 2030:

A Google Review from the Future

Evans Vista Neighborhood in the Year 2030

I moved to Evans Vista years ago and watched my new neighborhood blossom. It’s a homecoming. Many of my friends returned to Port Townsend due to the increased amount of affordable housing. The on-site daycare is a relief for working families. Affordable townhomes empowered struggling friends to become homeowners. This is a place where people succeed. The demand for the 321 available units led to a waiting list of current and former Port Townsendites, all yearning for a backyard where you can take tai chi lessons followed by garden-to-table kombucha workshops, and later a Chautauqua band finished out with late-night open-air movies….

Evans Vista personifies our local vibe. Diverse and affordable housing options cater to all. The abundance of open spaces, trails, community gardens, and gathering spaces promote individual and community health, fostering connections among residents. The mix of market-rate and affordable housing boast Port Townsend’s commitment to diversity and inclusivity….

Evans Vista is not merely a neighborhood; it’s a testament to what Port Townsend life should be. It’s a portal to the future where sustainable and inclusive havens thrive.

– Evans Vista Resident, May 1, 2030

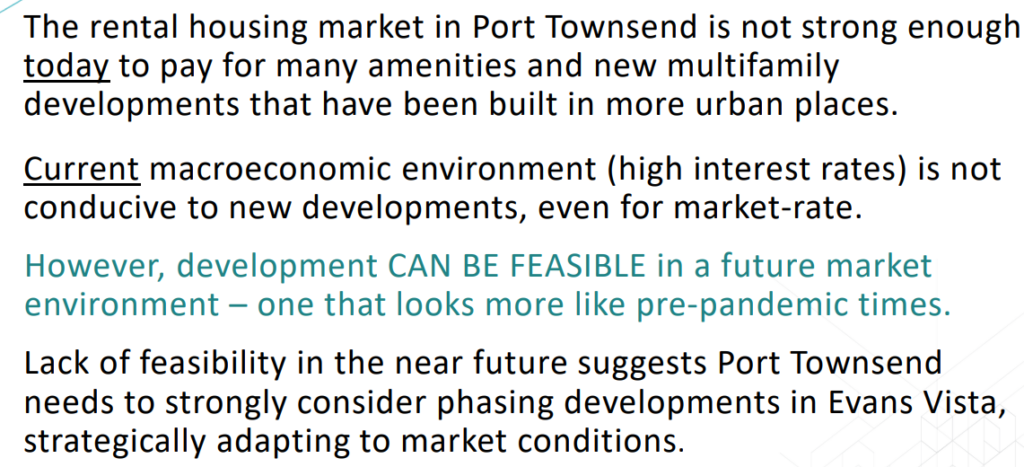

The reality check that followed the nice pictures brought spirits down fast. You could see the faces of city councilors drop (especially Mayor Faber, who may have been seeing that Cherry Street Project repeat he dreaded). According to economic analysts with ECONorthwest, there was no likely scenario in which the master plan could work. “A combination of factors need to change for the entire site to be feasible.”

Slide from ECONorthwest presentation

Those factors would be a deep cut in construction costs, much higher rents throughout the city so that higher rents could be charged at Evans Vista, and a return to pre-pandemic interest rates and market conditions like those in 2013. Failing a dramatic change in all those factors, the project does not “pencil out.” It is unfeasible even without any “affordable” units and with all units rented at highest market rates.

City council did not tell the architect to come back with a design that stood a chance of being built sometime soon. Instead, the council gave its unanimous approval to a plan that can’t be built.

To date, $2,149,942 has been spent on the project (right-hand column in table below) with millions more in the budget (left hand column).

Table of budget and expenses for Evans Vista project, from the city’s 2025 final budget

Three Strikes

Since the city acquired the Evans Vista property, dozens of people who had once found affordable (free) housing under the trees have been evicted. It cost about $100,000 to clear out their camps and cart away their refuse, with city staff providing the labor. A large chain link fence and “no trespassing” signs threatening criminal prosecution surround much of the land.

The people who used to live there moved not very far away. Some were accepted into the Mill Road homeless camp, officially named the Caswell-Brown Village after two homeless individuals who died from substance abuse. Many others have pitched tents in the woods and meadows north of the DSHS building on a city right-of-way and private property behind the Les Schwab store. I have been told by people who do outreach to the homeless that about 50 people could be living in that area.

Homeless encampment on north side of Evans Vista

Homeless camp on north side of Evans Vista, behind Les Schwab

Mill Road (Caswell-Brown) homeless camp

Blue marking at bottom left indicates approximate area of Mill Road camp; blue line at bottom right shows boundary of area occupied by homeless camps near DSHS building; Evans Vista property delineated by dashed red line.

The large Mill Road camp lies on the south side of the Evans Vista property. Every day some of its residents cross the Evans Vista property to get into town. I have been told of, but not seen for myself, another sizable encampment very near Evans Vista along a power line right-of-way.

Several years ago I wrote about the frequent law enforcement call-outs to the Mill Road camp due to drug dealing, substance abuse, thefts and assaults. Law enforcement sources speaking off the record inform me that the camp is being better managed now, with fewer calls to law enforcement. Drug use inside the dwelling units, however, continues and there have been several overdoses and other complications from substance abuse.

The camps at the other end of the Evans Vista property, near the DSHS building, and in the surrounding woods have seen a sharp rise in methamphetamine abuse. Those camps have become increasingly violent — so violent, according to law enforcement sources, that people have fled and set up camps along nearby power lines.

Moreover, immediately to the east of Evans Vista and the homeless camps is the odiferous paper mill.

Evans Vista is not exactly prime real estate, yet the analysts used rental rates at the fairly new West Harbor Apartments as a lodestar. Rents at Evans Vista would have to be higher than what is charged at a fairly up-scale complex in a desirable location.

Even an all-market rate project with NO subsidized “affordable” units would be unfeasible, according to ECONorthwest’s analysts, unless the city’s rental rates across the board go higher. How ironic, that in order to provide a limited amount of affordable housing at Evans Vista, housing would have to become less affordable for everyone else.

Higher rents alone would not make the project feasible. Interest rates would also have to drop very significantly. But rates have declined less than the predictions ECONorthwest presented to council in 2023. Thus far in 2025, the Federal Reserve has not cut interest rates. According to the minutes of the most recent Fed meeting, any cuts are on hold indefinitely while inflation persists.

Slide from ECONorthwest presentation

Two of the three factors necessary for any chance of the TAS design being feasible are not attainable. As ECONorthwest also discussed, assuming the TAS design remains the basic plan, there is little that can be done meaningfully to reduce construction costs. That makes three strikes against the Evans Vista Project.

How Could This Happen… Again?

In a few years time, Port Townsend has seen four big-vision, costly public works efforts flop: The Cherry Street Project. The golf course “revisioning” as P.T.’s Central Park. The mega-bucks Taj Mahal aquatic center. And now Evans Vista.

These projects share several attributes. First and foremost is that none of them are core municipal services, such as providing infrastructure and law enforcement — the fundamental reasons why municipal corporations are formed. Millions of dollars have been wasted that could have gone towards fixing the city’s streets and deteriorating sewer and water systems went to consultants or staff hired principally to drive home the golf course and pool projects.

The amount wasted is not insignificant. Recently, the century-old pipeline that brings water to Port Townsend suffered two major breaks. As the Leader reported, the 2025 repair budget for this critical infrastructure — P.T. can’t exist without it — was only $63,672. A single January water line break cost $150,000 to repair.