Gaping holes in the construction estimate for the proposed $37.1 million Port Townsend aquatic center translate into millions of dollars in future costs overruns, according to Mark Grant of Grant Steel Buildings and Concrete Systems, Inc. (see his bio below).

Mr. Grant grew concerned about the proposed Port Townsend aquatic center construction budget and did a deep dive as an act of public service. He discovered major omissions resulting in the project being seriously under-budgeted — meaning, additional costs and change orders down the road will result in significant cost overruns.

At the Brinnon public forum sponsored by the Port Townsend Free Press on November 21, 2023 he had the opportunity to brief County Commissioners Greg Brotherton and Heidi Eisenhour on his findings. Also in attendance at the meeting was Port Chairwoman Pam Petranek, Port Townsend City Council Member Ben Thomas and Quilcene Fire Commissioner Marcia Kelbon, as well as members of the public.

He later provided his analysis to County Commissioner Kate Dean in a separate letter.

Mr. Grant now shares his worrisome findings with the public. He begins by showing that the optimistic start and completion dates for the proposed aquatic center are years away from consultants’ estimates. This article is adapted from and expands upon his letter to Commissioner Dean.

— The Editors

——————————————

My budgetary concerns with the proposed new aquatic center project stem from my review of the current documentation available from both Opsis Architecture and DCW Cost Management (see report here). I am concerned that based on the current project site plans, floor plans, renderings and cost evaluation spreadsheets, this proposed project as currently estimated is significantly under-budgeted.

I have created an estimated schedule for this project based on my experience with projects that are municipally based, that require public and private funding, that require municipal bond acquisitions, and that are complex in nature. This schedule appears as the graphic at the top of this article.

A Realistic Construction Schedule

The DCW Cost Management Preferred Option – Cost Plan Update dated June 30th, 2023 doesn’t address the project schedule at all. On page 5 of this document, under the paragraph heading “Procurement,” there is a reference to “the start date is anticipated for Q1 2024,” with repeated references within the spreadsheet cost data of “Escalations to Start Date (Q2 2025).”

Their worst case scenario projects costs related to a delay in the start date to Q2 2025. The assumed start date information provided in the DCW report is not realistic given all the logistical steps needed to begin construction. It is my opinion that the political/voting, design, contractor procurement with contract negotiations, and permitting processes alone would push the potential start date out nearly two years.

For example, it is likely that the design approval process for the proposed Public Facility District (PFD) and the community approvals will take a full year. Likewise for the following phase which includes project bid solicitation with contractor selection, the submittal process, and contract negotiations.

The estimated schedule I show at top identifies that the realistic and likely start date for construction of the aquatic center as currently designed and proposed would not begin until late January to early February of 2027. This timeline is relative to my experiences with public works construction projects in general.

This would be followed by what I estimate to be a three-year construction process, moving the opening of the proposed facility out to early February of 2030. It may be possible to have an earlier completion date, but given the nature of public works projects in general, the complexity of the current design, as well as design elements that I feel are not represented appropriately with the current design information — i.e. site development — an estimated completion date in 2030 is justified and realistic.

The Budget

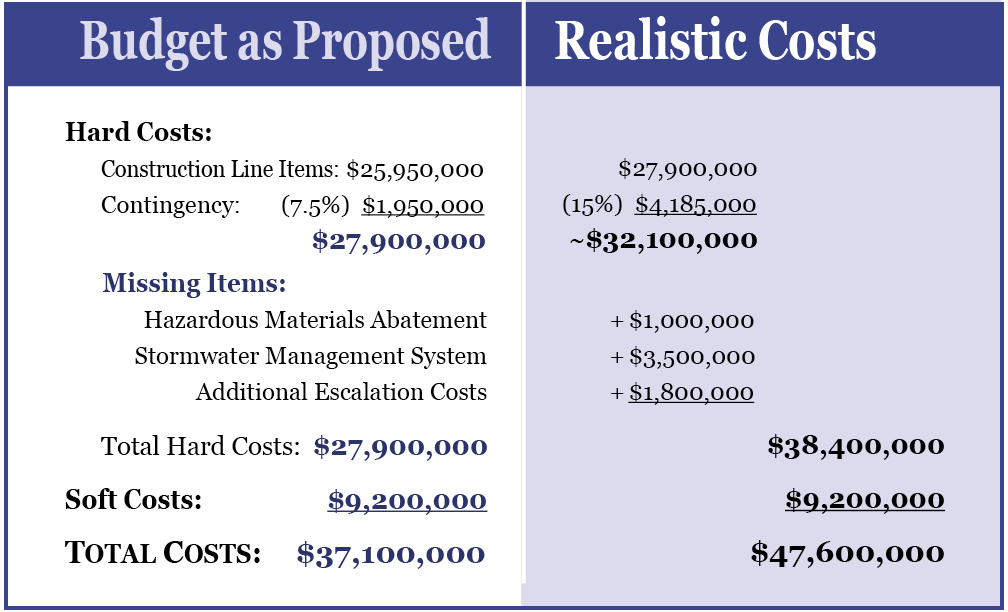

The current “for-construction” budget is listed as being $37.1 million. This amount includes both the soft costs at $9.2 million (for design, project management, permitting, third-party testing, etc.) and the hard costs at $27.9 million to construct the facility.

Underestimated Hard Costs

DCW’s $27.9 million includes contingency funds totaling $1.95 million (about $1.7 million for building-works line items plus $250K for sitework line items), leaving only $25.95 million in line-item construction hard costs. In reviewing the site plans, floor plans, and architectural renderings for the proposed facility, I found that the budgeted amount for hard costs was light. Based on my interpretation of the information provided by Opsis Architecture depicting a very complicated architectural design for the primary structure, with a complex clerestory multi-tiered timbered roofing design and elaborate finishes throughout, a difference of approximately $140 per square foot needed to be applied.

I also saw scope-of-work line-item omissions in the DCW cost analysis which I already assumed to be absorbed by the proposed contingency amount. These omissions should have been considered as line-item hard costs prior to any contingency money being applied.

The additional square footage costs and omissions in line-item hard costs effectively absorb the $1.95 million that had been included for contingency funds. That creates a $27.9 million base for hard costs before contingencies.

Inadequate Contingency Funding

The $1.95 million contingencies monies that DCW had allocated are significantly light; their 7.5% contingency is far below industry standards. With frequent material price escalations (now seemingly permanently embedded since Covid) as well as ongoing supply chain disruptions, the typical 10% contingency is becoming a thing of the past. It is being revised upwards to 12%-15% to manage the uncertainties and concerns of both owners and lenders.

Based on the project’s complexity and current design, I believe a contingency at a percentage basis of no less than 15% should be applied to the revised base construction costs of $27.9 million, which would be $4.185 million. This brings the project total estimated budget for hard costs to roughly $32.1 million.

Missing Hazardous Material Abatement Costs

To elaborate further, the demolition numbers are low in the DCW plan, especially in that no monies are allocated for hazardous materials abatement; the report states “No work anticipated” for this line item. This is a significant omission, as abatement will very likely apply given the age of the existing facility and the materials that were used back then for construction.

The hazardous materials abatement cost could be as much as $250,000 to $1 million, depending on the types and amounts of materials likely to be found. The higher amount added to the $32.1 million brings the hard costs up to $33.1 million.

No Stormwater Plan

Construction of the stormwater system needed to accommodate the large surface areas shown — for what would be considered to be impervious surface impacts for the parking, sidewalks, buildings, etc. — will require a substantial system design for stormwater management as required by the currently adopted Washington State Stormwater Manual. This system will require treatment/filtration, detention/retention, flow controls, and a design for overflows.

The existing soils at the Mountain View site are not conducive for infiltration, as glacial-till/hard-pan conditions are present below the thin layer of organic top-soil type material, which do not accommodate infiltration. The system designed could cost $1.25 million on the low side, and may even cost as much as $3.5 million.

The DCW plan shows a line item for storm sewer costs at $150,000 as an allowance. Note that any items in a cost analysis listed as an allowance imply there was not enough information/research done to determine the true costs, which makes these line items susceptible to huge change-order activity during construction, which would need to be paid for by the owner.

Therefore, a $3.5 million stormwater system added to $33.1 million brings the new total estimate for hard costs to $36.6 million.

Realistic Escalation Costs

The current budget also includes cost escalation funds (adjustments for future construction cost inflation) on materials and labor carried out only to 2025. As described above, that time frame is unrealistic.

The unrealistic 2025 start date indicates to me that the currently budgeted cost escalations are potentially significantly inaccurate and need to be revised to reflect a start date two years later than as proposed. There are too many issues that could significantly affect higher costs on materials and labor looking towards 2027, so it is reasonable to assume that costs will be higher.

Failure to adjust the cost escalations to match a realistic construction schedule means that likely construction cost increases are not included in the construction budget.

Escalation costs that are tied to the hard cost for construction are important to consider, but could/should be considered speculative. Although uncertain because the time the escalation occurs and economic factors are both unknowns, based on my experience it is reasonable to assess an additional $1.8 million for this project given a more realistic 2027 start date.

That makes the final total for hard costs $38.4 million.

Adding It Up: A $47.6 Million Pool

Adding the more realistic $38.4 million in hard costs and $9.2 million in soft costs brings the estimated total project cost to $47.6 million. That is a potential $10.5 million of extra costs to cover, which should be very concerning.

It is my opinion that the project feasibility should be based on this revised $47.6 million amount, not the $37.1 million as is currently proposed.

How does that amount figure into the proposed 0.2% increase in sales tax revenue needed to fund the facility construction, service the debt, and pay for some of the proposed operational expenses year over year?

Finally, money for contingencies in a project budget is not supposed to serve as a stop-gap for not performing thorough due diligence for the initial project design considerations. My concern is that this initial budget analysis (as provided to review project feasibility) has holes and does not present reliable project budget cost information for moving forward with a new capital facilities project/campaign, let alone the formation of a new taxing district to support it.

The best approach to complete this proposed project, or any project, is to ensure that there is enough money available without having to either make project cuts or go out for more funding resources, i.e. the taxpayers. If this project were to move forward based on the currently budgeted cost information, I am concerned that — with inevitable cost overruns and debt needing to be serviced — the only way out for the newly-formed Public Facilities District would be through a property tax increase, meaning the county-wide property taxpayers will have to serve as the guarantors for the initial debt secured.

Where else is the money for these potential construction cost overruns, debt servicing, and even operational expense shortfalls going to come from?

Mark Grant has operated Port Townsend’s Grant Steel Buildings and Concrete Systems, Inc. since 1995. His company built the 32,000-square-foot Aero Museum and the administrative offices for the Port of Port Townsend. He builds commercial, residential, industrial, agricultural and public works projects of various sizes and magnitude. His clients include the City of Port Townsend, Port Townsend School District, Jefferson County, City of Bremerton, Washington Department of Corrections, United States Geological Survey and the U.S. Department of Defense/Navy.

Even worse, $10.5 million extra hard costs and 3 extra years before starting construction would have significant downstream consequences. Total debt service on the extra $10.5 million at 6.3% interest rate over 25 years would cost another $10.4 million, which added together boosts expected 25-year pool costs from $108.9 million up to $129.8 million.

Moreover, the later 2027 start date would delay the day when (best-case-scenario) the pool could become operationally solvent, increasing risk of default on loan payments during its first years without a larger reserve fund (requiring even more debt to finance).

These problems were detailed in “The $108,941,000 Pool Could Default Its First Year“, except the situation that article described is accentuated by the additional costs and delays uncovered here.

I have known Mark for 20 years and I will vouch for his veracity. He has completed many projects around this area including the Twisters Gym facility in Hadlock and many others, well documented. He is a quality analyst with his multi year construction experience in comparison with the consulting firms hired by the pro pool/spa/resort group.

Richard Thomas.

Sir-

Thank you for your time, expertise, and service. Public servants these days are not employed by the government.

In tide pools and petri dishes large and small.

I just came across this article which I thought was interesting since it is a similarly sized county [population-wise] to us. However, they used a different approach by actually saving funds in advance and retrofitting the existing building while it was still open. https://www.tillamookheadlightherald.com/news/construction-progresses-on-new-ncrd-pool-building/article_3f03d4b2-a037-11ee-b3d3-6373b5a27eae.html?utm_campaign=blox&utm_source=facebook&utm_medium=social&fbclid=IwAR3XNYpkdgCFRZ5or8XcmeHtHLe4lNkfzx7nBqkQsxFXhd5stpRqkWAnSbs

Ashland, OR $10 mil new public pool proposal

https://www.rv-times.com/localstate/new-enclosed-city-pool-in-ashland-could-cost-10-million/article_59c74592-ae5e-11ee-8cc2-7fffe6c9d579.html

The Daniel Meyer Pool project in Ashland could cost as much as $10 million and will likely include an enclosure.

That was the gist of a Parks & Recreation Commission study session last Wednesday where the pool project was the focus of a long discussion. Originally budgeted at $5.5 million in design estimates created in 2020, APRC staff have raised the budget to $10 million to accommodate for inflation and rising construction costs with the hope the final project will come in under that budget, said Interim Parks & Recreation Director Leslie Eldridge……..